Pocket money in New Zealand: how much, when to start, and how to run it

Most pocket money advice online is American — dollar amounts that don't translate, allowance culture that doesn't quite match how Kiwi households run, and product pitches for US debit cards you can't get here. This is the NZ version, from a Kiwi dad who builds a chores-and-rewards app and has had every one of these arguments at his own kitchen bench.

When to start

Around age five or six is the sweet spot — once kids can count coins, want things at the dairy, and can connect "I did the job" with "I got the money". Before that, money is just shiny tokens; points, stickers or star charts do the same work with less to lose down the back of the couch.

The better question than "what age" is "what trigger": start when your kid first asks you to buy something non-essential more than once a week. That's the moment "we'll see" can become "you've got pocket money — is it worth it to you?" — which quietly moves the negotiation out of your head and into theirs.

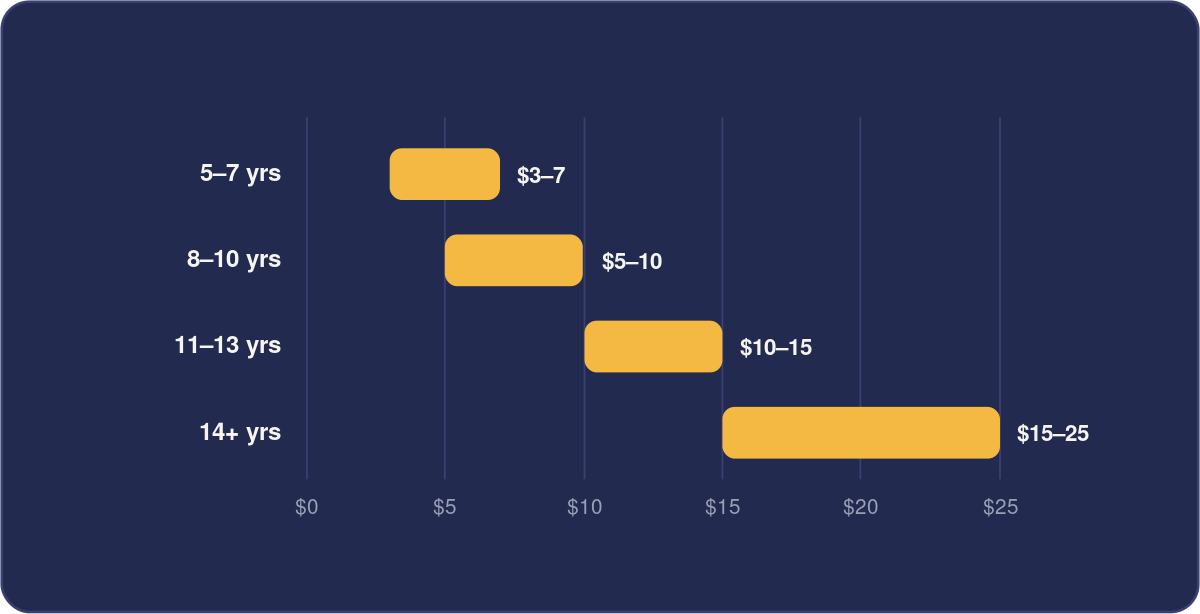

How much (in actual NZ dollars)

There's no robust national survey of NZ pocket money rates — anyone quoting a precise "Kiwi average" is mostly guessing. But the rule of thumb that keeps showing up among NZ parents and banks' money-skills guides is roughly 50 cents to $1 per year of age, per week:

- 5–7 years: $3–$7/week — enough for a small treat decision, small enough that blowing it all teaches cheaply

- 8–10 years: $5–$10/week — introduce a save/spend split here

- 11–13 years: $10–$15/week — they start covering some of their own wants (game credits, mall trips)

- 14+: $15–$25+/week, often restructured as an "allowance with responsibilities" — they manage their own top-ups, gifts for friends, some clothing

Calibrate to your household budget without guilt — the system teaches the money skills, not the amount. A consistent $5 beats an erratic $15 every time.

Tie it to chores or not?

The genuinely contested question. The short version (the long version, with the research, is here): a three-tier hybrid wins for most families. Some jobs are unpaid because you live here; a middle band of real contribution earns the money; big one-off jobs get negotiated at premium rates. Pure pay-per-chore lets kids opt out of helping whenever they're flush; pure unconditional allowance disconnects money from effort entirely. The hybrid keeps both lessons.

Cash, kids' cards, or points?

Cash is tangible and great for under-eights — but it needs you to actually have change on Sunday (you don't), and it teaches nothing about the invisible digital money kids will really use.

Kids' debit cards (SquareOne is the local one; banks offer under-18 accounts with Eftpos cards from various ages) make real spending real. They come with monthly fees in some cases, and a card plus app is a lot of machinery for a six-year-old earning $4 a week. Sensible from intermediate age up.

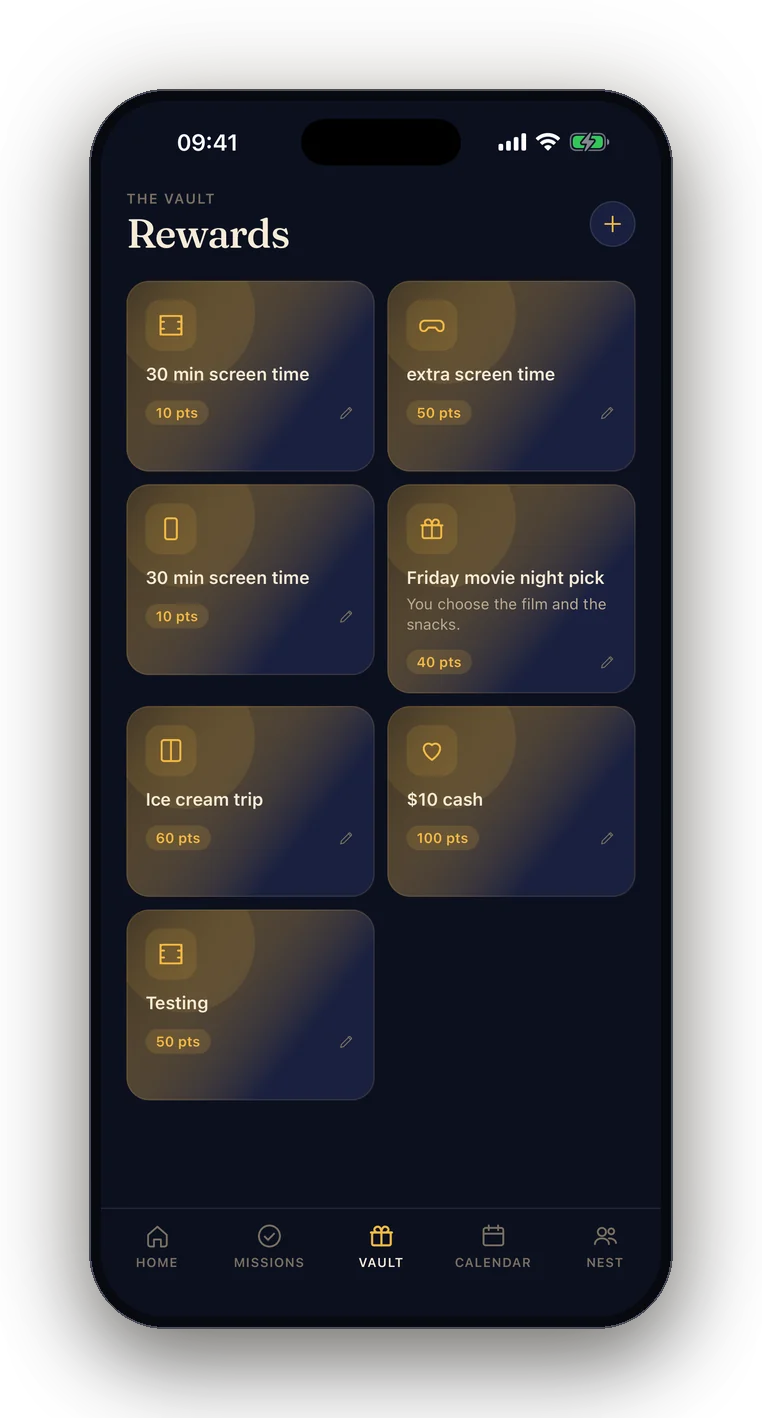

Points first is our honest recommendation under about ten — and not just because we make a points app. Points pay out the moment you approve the job (no Sunday float required), they buy more than money (screen time, movie night, staying up late — often stronger motivators than $2), and a points balance saving toward a big goal is delayed-gratification training with zero banking admin. Then graduate to a card once real-world spending starts: points for the home economy, card for the street economy.

The save/spend/give split, without the eye-roll

The classic three-jars advice survives because it works — just keep it proportional and light: most for spending (the motivation), some for saving (the lesson), giving optional but offered (the values). With points, "saving" is simply a big savings goal — the $60 Lego set at 600 points does more for patience than any lecture about compound interest.

Keep it boring (that's the secret)

Whatever you choose: same rates, same payout day, no retroactive renegotiation, and never quietly bail them out mid-week. Pocket money teaches by being predictable — a tiny, friendly economy where the rules hold. Kids don't need the rates to be generous; they need them to be real.

FamOwl runs your family's points economy — missions earn points, and rewards pay out in screen time, treats, or pocket-money cash-outs at rates you set. Built in New Zealand, free on the App Store.

Get FamOwl freeSome FamOwl articles are drafted with AI assistance and reviewed by our team. They're general information, not professional, financial, or medical advice — every family is different, so use your own judgement. FamOwl isn't liable for decisions made based on this content.